Every year

banks and building societies take nearly £2 billion straight out of the savings

accounts of millions of their customers and pass it on to HM Revenue &

Customs. They do this without asking or checking if those customers are

taxpayers or not. Half the UK population does not pay income tax. The result is

that more than £200 million is given to HMRC which should never have been taken

at all.

Don’t blame the banks and building societies. They are obliged to hand

HMRC this annual windfall. And for ten years HMRC has made no little effort to

give it back. The last campaign appealing to everyone was in 2004. It got very

little response as did targeted messages to low income pensioners in 2008 and

2009. Thirty million people in the UK – young and old – do not pay income tax

and many of them have savings. But HMRC happily taxes them unless they ill in the right form to ask it to stop. And doesn't repay tax it shouldn't have had until they fill in another form - one for each year the great tax take applied.

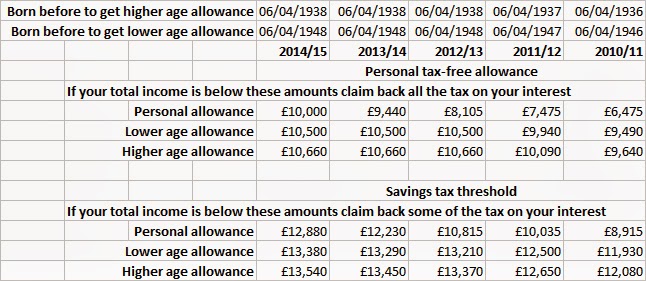

In 2014/15 you can have £10,000 income without paying a penny of income tax. If you were

born before 6 April 1948 the amount is slightly higher – £10,500 for those born

April 6, 1938 to April 5, 1948 and £10,660 for anyone born before 6 April 1938.

These allowances are personal – so it does not matter what income your wife or

husband may have. If your total income is at or below that level then you

should pay no tax on it and every penny of interest your savings earn should be

tax-free. But unless you fill in the correct form tax at 20p in the pound will

be deducted from that interest automatically.

A lot of the people affected are

over 65. But there are also children, teenagers, low paid workers, full time

mothers, non-working spouses, people with illnesses or disabilities, in fact

anyone of any age with an income below the £10,000 personal allowance who has

savings. HMRC gets some of their savings interest whether they should pay it or

not. It gets at least £200 million a year it should not have and it may be a

lot more.

To stop HMRC

getting this annual bonus you need to fill in a form called Form R85. You can

download it from the gov.uk website – just put ‘tax on savings interest’ in the

search box of that site and scroll down to find it. Fill it in and give it to

the bank or building society which holds your savings. You will need one for

each. Some current accounts pay interest so they will need one too. That will

stop this tax being wrongly taken in future.

Next you

have to claim it back for previous years. You need another form called Form R40 from

the same web page. You need one for each year back to 2010/11. In those years

the amount of income you could before tax is due was lower – just £6475 for

those under 65 in 2010/11. But if your income was low enough you could claim

tax back from those years too.

You will get back one quarter of the net interest

your savings have earned in those years. It could be hundreds of pounds. Fill

in the forms and send them to HMRC, Leicester & Northants (Claims), Saxon

House, 1 Causeway Lane, Leicester LE1 4AA. In a few weeks you should get a

cheque refunding the amount wrongly taken – plus a small amount of interest on

it.

Dolly is 61

and has not worked full time since she was made redundant at 55. She has a

couple of part-time jobs locally but she is lucky if she earns £150 a week. Her

£30,000 redundancy money is sitting in a fixed term savings account where it

has been for some time and earns her around £1000 a year. But she is left with

just £800 after HMRC snaffles £200 of this. She decides to claim the over paid

tax back to 2010/11. She is owed even more for the earlier years when rates

were higher and before she took out the fixed rate bond. She even claims the bit of tax paid from April

to June this tax year as well. And she registers with the bank to have the

interest paid gross in future. So she gets nearly £1000 back from HMRC and is

£200 a year better off in future.

Even more

tax back

There is

another tax refund that some people with savings could get even if their income

is a couple of thousand pounds or so above the personal allowance. Savings

income just above the personal allowance is taxed at a lower rate – 10p in the

£ rather than 20p in the £. But it is still deducted by banks and building

societies at the full 20p.

It works

like this. Interest on savings is like cream – it floats on top of the rest of

your income such as pensions or earnings. So if that other income takes up all

your personal allowance or a bit more the savings interest that floats on top

of that is taxed. But if it is within £2880 above your personal allowance the

tax rate on it is only 10% (called the starting rate) instead of the basic rate

of 20%. So half the tax taken automatically should be refunded.

Violet is

75. She has state and private pensions totalling £11,500 a year. And interest

from her £50,000 which is £1000 this year. That is above her personal allowance

of £10,500 so she pays some basic rate tax on £1000 of her pensions. But the

£1000 interest takes her income only up to £12,500 and that is within the

£10,500+£2880=£13,380 limit for the starting rate band. So the £1000 of

interest is taxed at 10% not 20%. In other words she should pay £100 tax on it

not the £200 that was automatically deducted. She can claim this back using form

R40. She can also claim back for previous years as the £10,500 allowance has

not changed for people of her age for some time. Altogether she should get

several hundred pounds.

You claim it

back using the same form Form R40. If you have some savings income and your taxable

income is £12,880 or less then you can claim back half the tax taken on the

savings. If you were born before April 6, 1938 it can be as high as £13,540 and

£13,380 if you were born 6 April 1938 to 5 April 1948. Previous years

allowances and bands are set out in the table.

{kind=link}

This story first appeared in Saga Magazine April 2014.

Published here with updates and amendments 8 March 2015

vs 1.00

vs 1.00